Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form

In spite of the long Easter weekend, the PMAX market trended upwards on the back of fresh cargo orders coming from ECSA and the Pacific region. Iron ore and coal trades remained strong and the supply of tonnage remained steady. PMAX vessels on a DOP basis opening in South China heading from Indonesia to China were rating around the low $11,000s/day. Additionally, PMAX vessels on a DOP basis opening in North China heading from Australia to China and Australia to India were around the low $10,000s/day and mid $10,000s/day respectively. The market out of EC Australia sees little activity as the effects of Cyclone Debbie linger. However, the pause in Australian coal supply has reinvigorated NoPac business, particularly on the metallurgical coal stems as Indian and Chinese charterers try to cover their shortfall.

Despite fairly strong gains in the North Atlantic and US Gulf SMAX, the market in the Eastern basin lacked last week's vigor. As Chinese coastal freight rates moved lower, tonnage lists swelled up w-o-w forcing owners with vessels open in the CJK/North China region to scramble for coal and steel shipments into India and iron ore cargoes out of Western Australia. A trip to WCI from Korea basis North China delivery for a 58,000 DWT was paying around low $10,000s/day and low $5,000s/day to SKAW-CONT from Korea basis CJK delivery. A SMAX doing a NOPAC round voyage on a DOP basis opening in Korea/Japan was in the mid $9,000s/day range. Short period enquiry was more or less the same as last week but rates are now hovering in the $9,500-$10,000/day range.

Pre-monsoon coal stocking by Indian traders continue and market chatter regarding the recommencement of nickel-ore shipments out of Indonesia have resurfaced. A few enquiries for SMAXs for gypsum out of China to the Philippines and slag from Indonesia to Bangladesh were heard. Yet, the aggressiveness of a few Chinese owners/operators to capture non-China discharge related business pushed the market lower. SMAX vessels on a DOP basis opening in Singapore/Southeast Asia heading from Indonesia to India and China are in the mid $10,000s/day and high $9,000s/day range respectively.

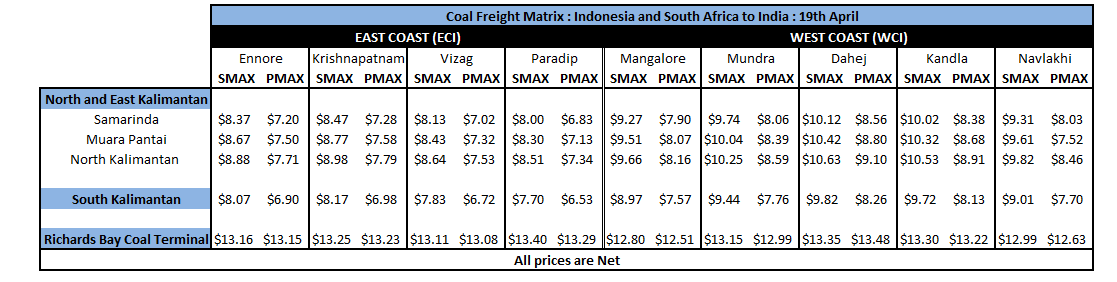

The market in the Indian Ocean moved sideways w-o-w as the positive impact of an active ECSA market was nullified by lacklustre trade flows out of South Africa (due to an increase in coal prices) and the Persian Gulf. SMAX on a DOP basis opening in ECI/WCI for the RBCT to India coal route rate in the low $9,000s/day range, while the PG to India route is currently around the mid $12,000s/day range. PMAX vessels on a DOP basis opening in ECI/WCI doing the RBCT to India route are around the low $14,000s/day range.